MBW Reacts is a sequence of analytical commentaries from Music Enterprise Worldwide written in response to main latest leisure occasions or information tales. Solely MBW+ subscribers have limitless entry to those articles. The under article initially appeared in Tim Ingham’s newest MBW+ Assessment e mail, issued solely to MBW+ subscribers final week.

Socialist French politician Aurore Lalucq is the co-founder of Tax The Wealthy, which desires to raid the belongings of rich people to fund “local weather transition” in Europe.

She’s additionally known as for the magical deletion of over $2.5 trillion (!!) in Eurozone authorities debt from the books of the European Central Financial institution.

Politically talking, she’s AOC as an MEP.

Now, Common Music Group is in her crosshairs.

On April 4, Lalucq known as on EU competitors chiefs to scrutinize Common’s proposed $775 million acquisition of Downtown Music Holdings, suggesting that it’d reward UMG “unprecedented management over routes to market”.

Her feedback had been cheered by indie label group IMPALA, which is seeking to snowball momentum in opposition to UMG’s Downtown deal in Europe. IMPALA claims that UMG’s buyout of Downtown – following the key’s latest buys of [PIAS] and 8Ball – will allow it to “gatekeep market entry”.

Regardless of these protestations, I predict UMG’s purchase of Downtown will breeze by way of with out regulatory intervention worldwide – and never simply due to as we speak’s Trump–influenced, anything-goes enterprise atmosphere.

Right here’s why…

1) Common is way from a monopoly

Market share sizing is all the time a harmful sport within the music enterprise, so let’s preserve this straightforward.

In keeping with IFPI, the commerce revenues of the worldwide recorded music rights trade (i.e. gross sales plus streams plus music licensing) amounted to USD $29.6 billion in 2024.

Common Music Group’s reported turnover from the identical revenue sources final 12 months hit EUR €8.90 billion, equal to USD $9.63 billion.

That’s a worldwide market share, on a commerce income foundation, of round 32.5%.

By my estimates, utilizing knowledge from UMG’s newest annual report and IFPI figures, Common’s market share in North America final 12 months sat at round 42%. In Europe (together with the UK), it was nearer to 31%.

These numbers are merely not giant sufficient to set off monopoly considerations.

Within the US, the Federal Commerce Fee states that antitrust courts usually have to see an organization personal a market share of 50% or above to even take into account if it workout routines “monopoly energy”.

In the meantime, the European Fee says, “If an organization has a market share of lower than 40%, it’s unlikely to be dominant.”

Common Music Group is comfortably under these thresholds, and the addition of Downtown brings no hazard that it’s going to exceed them.

(UMG’s market share in Asia and Latin America is significantly decrease than its equivalents within the US and Europe – which is why I’ve predicted a raft of M&A exercise from the corporate in these areas within the years forward.)

2) Unbiased music possession is flourishing

Whose facet are you on: David or Goliath?

That is an age-old argument from indie label reps when attempting to hobble main music firm growth.

However within the trendy age, issues get sophisticated.

Common Music Group is already paying out ten-figure sums yearly to copyright-owning artists and unbiased labels as their distribution/companies accomplice. (UMG primarily delivers these royalties by way of Virgin Music Group.)

So, positive, in the event you like, it’s David vs. Goliath.

However provided that Goliath’s pockets are filled with envelopes of money – destined for the letterboxes of David’s fellow indie villagers.

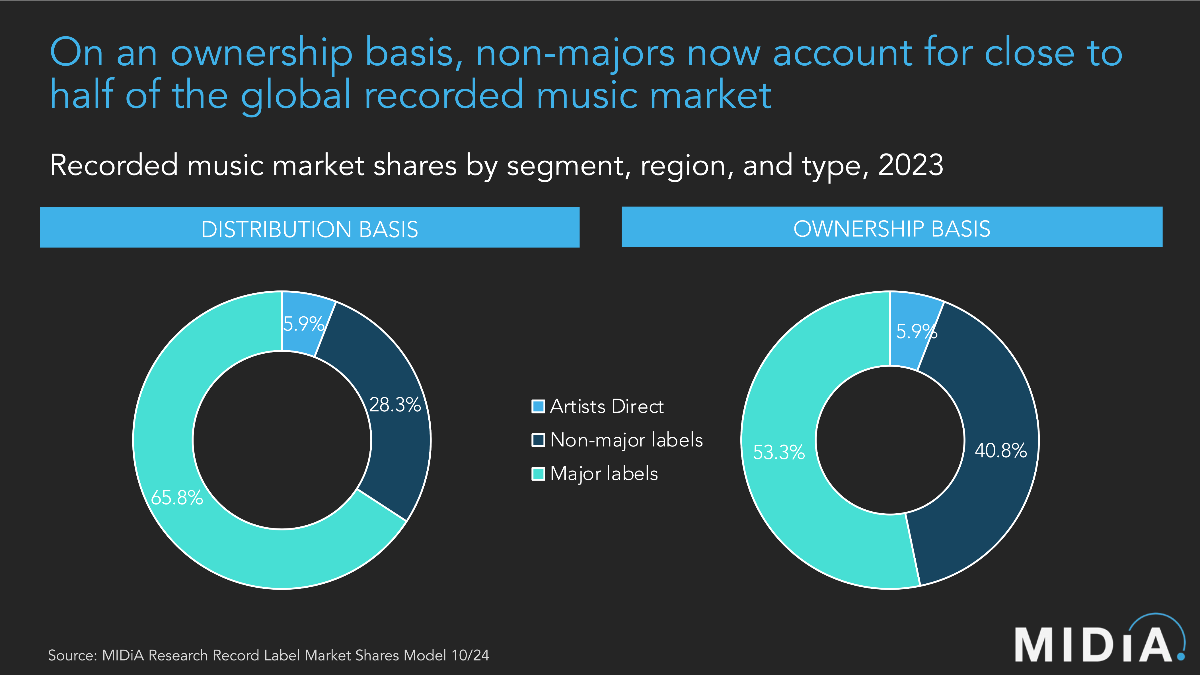

This brings us to the strongest argument for Common’s Downtown acquisition to cross regulators: in music, there’s a essential distinction between ‘distributed‘ market share and ‘owned’ market share.

In keeping with Midia Analysis, the three ‘majors’ (Common, Sony, and Warner) collectively declare round 66% of world recorded music commerce revenues on a distribution foundation, leaving the indies with simply 33%.

But on a copyright-ownership foundation, unbiased artists/labels declare a whopping 47% of the worldwide market.

Midia’s numbers suggest that round 20% of recorded music income on the three main music corporations is collected on behalf of copyrights they don’t personal.

In UMG’s case, in 2024, that ~20% would have equated to almost USD $2 billion.

As soon as collected, UMG would have paid the majority of this cash again to indie distribution shoppers.

In shopping for Downtown, Common is buying an organization with zero owned copyrights. (Downtown bought its music copyright catalog to Harmony for $400 million a couple of years again, after which it reworked right into a ‘pure service’ enterprise engaged on behalf of indie artists, songwriters, and labels.)

So not solely will the addition of Downtown solely trigger a minor share shift in UMG’s world distribution market share, it’s going to even have zero affect on UMG’s market energy as a copyright proprietor.

3) Unbiased music distribution is flourishing

In gentle of the above, IMPALA is cautious to argue that – following its acquisition of Europe-based distributor [PIAS] final 12 months – UMG’s buyout of Downtown will result in unfair focus in music distribution.

But even that is indifferent from the fact.

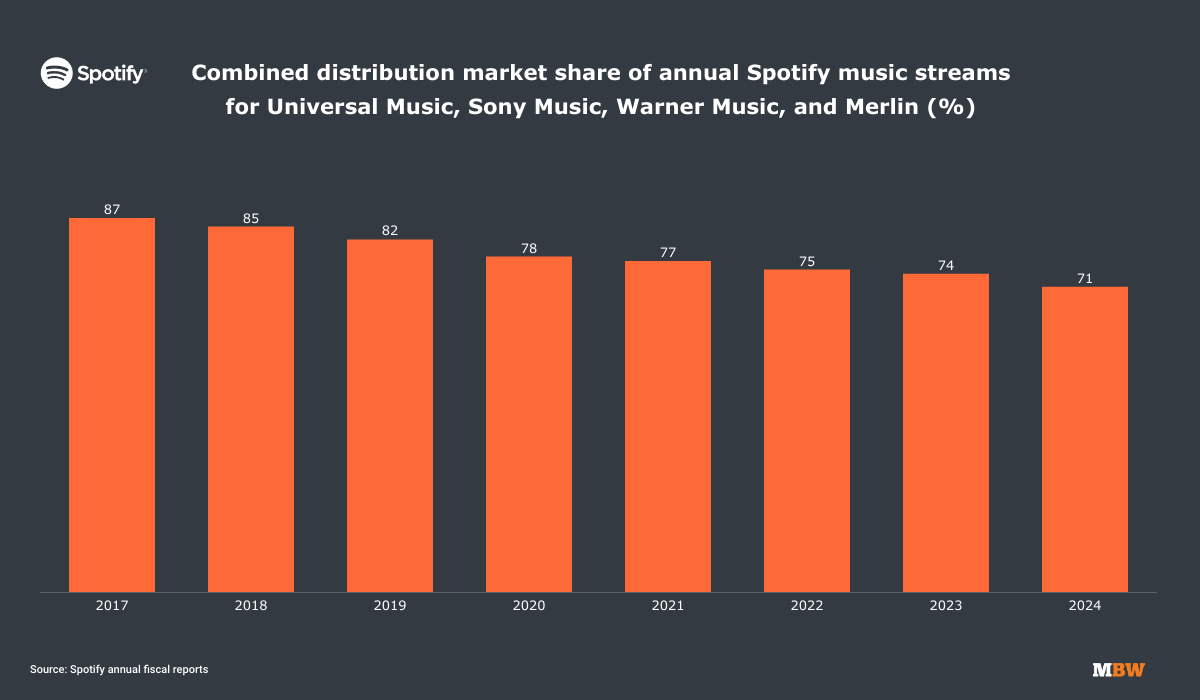

Those that prefer to see the majors get a kicking usually level to the chart under, which reveals how the majors’ distribution market share, plus that of indies repped by Merlin, has fallen by double-digits on Spotify over the previous decade.

This major-market-share decline has predominantly been pushed by two elements:

(i) The massive leap in consumption of unbiased artist/label music in markets like Europe, MENA, India, Latin America, and South Korea; and

(ii) The emergence of strongly monetized, self-distributing corporations exterior of the majors – from Consider to EMPIRE, Create Music Group, and gamma. (All of whom, by the way in which, are both price, or have raised, in extra of a billion {dollars}.)

Two of the most important music corporations on the planet, BMG and Harmony, are additionally now able to self-distribution: BMG by way of its direct relationship with Spotify and Apple, and Harmony by way of its latest acquisition of Stem.

The purpose? Not solely is Common now paying out billions to indies yearly as a distribution accomplice, however these indies (a) have full freedom to depart UMG and transfer their catalogs elsewhere, and (b) have a plethora of highly effective opponents to select from – that stretch far past Downtown.

Some within the indie sector have raised explicit considerations over the truth that, by buying Downtown, Common may even take possession of FUGA, a B2B content material supply platform, and Curve, a royalty processing platform. Each have direct relationships with many key independents.

However right here, too, you’ll discover strongly monetized opponents: Audio Salad, for instance, rivals FUGA, and is owned by SESAC/Blackstone. In the meantime, Tone – initially a part of Stem – competes with Curve and has been backed by billionaire Jack Dorsey’s Block Inc.

4) Common’s EMI acquisition in 2012/2013 didn’t create an almighty monopoly, in any case. In actual fact, EU regulators in all probability received it improper.

13 years in the past, egged on by outraged unbiased music lobbyists, Europe’s regulators dramatically did not predict the trendy world. A world wherein Common – and its thirty-something-percent world market share – battles an onslaught of formidable unbiased distribution rivals.

In 2012, mentioned watchdogs compelled Common Music Group to divest an unlimited chunk of catalog from its USD $1.9 billion acquisition of EMI Music. (This divestment grew to become Parlophone Label Group, which Warner purchased the next 12 months for round USD $765 million.)

In doing so, the European Fee swallowed arguments that the EMI deal would additional UMG’s “monopolistic place” in music, and would result in Common gaining an invulnerable market share of over 50% in key territories just like the UK.

Unsuitable, improper, improper.

In actual fact, because of sturdy competitors and the fast globalization of music streaming, Common has ended up controlling a smaller piece of a a lot bigger worldwide market.

Music & Copyright knowledge means that in 2013, contemporary from its EMI acquisition, UMG’s world distribution market share hit its peak at 39.7%.

Ten years later, in 2023, because of the rise and rise of non-major distribution, that quantity had fallen to 32.4%.

These statistics ought to embarrass Europe’s regulators, highlighting their lack of foresight into the place the music market was actually headed throughout that 2012/2013 EMI Music acquisition course of.

It’s a compelling, data-driven argument: Europe’s demand that UMG divest Parlophone Label Group in 2013 was an act of misguided regulatory overreach, led by doom-mongering forecasts that – we now know – had been wildly inaccurate.

I’d count on regulators to be doubly doubtful of the identical arguments this time round.

Music Enterprise Worldwide